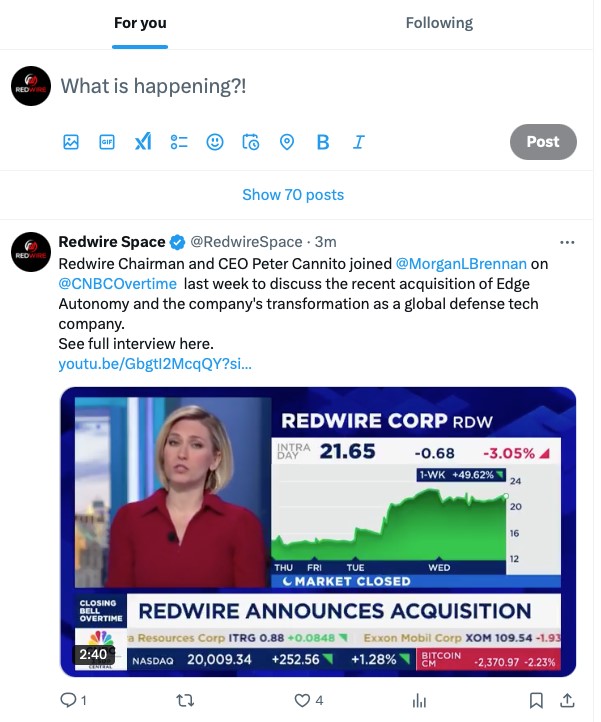

On January 27, 2025, Redwire Corporation distributed videos of a CNBC interview with Redwire President, CEO and Chairman, Peter Cannito, including the broadcasted and full interview by publishing posts on each of the media platforms; X, Facebook, and Linked-In. Below includes the posts published on each aforementioned media platform and transcripts of the interviews.

CNBC Overtime Interview - Broadcast

January 22, 2025

Presenters

Morgan Brennan, CNBC

Peter Cannito, Redwire President, CEO & Chairman

Jon Fortt, CNBC

Morgan Brennan

Another space stock that’s on the move this week – Redwire. Shares sliding today after the space company stock shot up 50% yesterday on deal news. Redwire, which bioprints organs in space and supplies parts to satellites announcing it will acquire aerial drone maker Edge Autonomy for $925 million dollars in cash and stock.

Now Redwire’s CEO Pete Cannito says national security work is already Redwire’s fastest growing business, but Edge Autonomy expands the company’s role as a defense tech company beyond just space.

Peter Cannito

This is Redwire leaning into that idea of being a multi-domain company of both space and autonomous airborne platforms. And if you think about what we did with our last acquisition of Hera, where we brought in these additional autonomous space-based platforms, now we’re adding the autonomous aerial platforms and the goal would be longer-term for us to build system-of-systems where these autonomous spacecraft collaborate with autonomous airborne platforms in order to realize that vision of an all-domain warfighting concept.

Morgan Brennan

So, Redwire won a Pentagon contract last year to build what is essentially an orbital drone and that really helps spur this strategy to create a one-stop shop for “platform” coverage, so think enabling those unmanned systems to collaborate and share data from the surface of the Earth to the surface of the Moon and beyond.

Now Edge Autonomy which has drones deployed in places like Ukraine that adds the Earth part for Redwire. At a time when space stocks have been soaring though and startups like Voyager Technologies may now go public, I asked Cannito what navigating Wall Street has entailed.

Peter Cannito

Elon Musk kind of helps us out with that, obviously he’s very visible in the community and so I think there are a lot of people in space right now and that public knowledge is certainly a tailwind for Redwire, because I think that the public writ large is more aware of what’s going on in space than ever before. I mean, I think it’s just consistently going out there quarter after quarter and educating people on what you’re doing and then delivering on the things that you say you’re going to do and we believe that if we continue to do that, that people understand it over time.

Morgan Brennan

With Edge Autonomy, which the deal is expected to close in Q2, Redwire will realize stronger topline and EBITDA growth and become cash flow positive. But Cannito is also not ruling out more acquisitions in the future, so check out the full interview on CNBC.com you can also check out my podcast Manifest Space. John, Redwire shares up almost 640% over the past twelve months.

John Fortt

Cool stuff, yeah.

CNBC Overtime Interview

January 22, 2025

Presenters

Morgan Brennan, CNBC

Peter Cannito, Redwire President, CEO & Chairman

Morgan Brennan

Joining me now, Peter Cannito, the CEO of Redwire and fresh off of the news that you are acquiring Edge Autonomy. Let's talk a little bit, let’s start right there. This acquisition, it takes you into defense tech. Why the acquisition? Why now?

Peter Cannito

That's a fantastic question. So, Redwire is already in defense tech, quite frankly. We do work for national security already in space and it has been, in fact, in our most recent history, the fastest growing area of our business. So this is really just underscoring and leaning into that trend.

Morgan Brennan

So it takes you into another domain, I guess I should say. I always think of you as a space company, a space infrastructure company, but this expands your reach into drones and airborne systems.

Peter Cannito

That's right. So it's expanding into a new, really complementary domain. Right? So if you look at where our customer has been heading in terms of our national security customers, they're focused on a joint all-domain strategy, what they call JADC2, Joint All-Domain Command and Control. And so what this does is, this is Redwire leaning into that idea of being a multi-domain company of both space and autonomous airborne platforms.

And if you think about what we did with our last acquisition of Hera, where we brought in these additional autonomous space-based platforms, now we're adding the autonomous aerial platforms and the goal would be

longer-term for us to build system-of-systems where these autonomous spacecraft collaborate with autonomous airborne platforms in order to realize that vision of an all-domain warfighting concept.

Morgan Brennan

How revolutionary is it to see that communication happening between domains? I have a lot of conversations about JADC2, which outside of, I think defense circles is one of those wonky acronyms that doesn't always fully break down or reflect perhaps the graveness or importance of this concept.

Peter Cannito

Well, it's an incredibly important concept. I mean, it's that technological edge that underpins the power of U.S. national security, and space has always been one of the critical pillars where the U.S. has really been at the forefront in terms of national security. Now expanding that dominance in space to be integrated with the other domains like air, sea, and ground really provides an incredible strategic advantage. For Redwire to have two of those domains vertically integrated in a highly agile middle-market company like us, we believe is going to be really appealing to our customers and positions us, quite frankly, in a very unique way in the market.

Morgan Brennan

And what does that market look like? How does it evolve?

Peter Cannito

Well, I think the way it evolves is as you start to be able to show that collaboration between autonomous platforms, the customer set looks to buy from those who can make that as seamless and as simple as possible. And we’ll be really well-positioned to take advantage of that trend over time.

Morgan Brennan

How did the deal come together? I'm curious about this, because I know you said you wanted to expand your reach within defense previously. Redwire is a company that was born out of AE Industrial and Edge Autonomy was born out of AE Industrial as well. So both, I guess portfolio or former portfolio companies.

Peter Cannito

That's right, that's right. Obviously we were aware of each other as organizations, and therefore have been able to watch each other develop and quite frankly, follow similar paths from a scaling perspective. So that always obviously makes a deal easier when you already have a pretty strong understanding of each other's teams, of each other's cultures, of each other's growth success; but it really started with Redwire's entry into the very low Earth orbit, or VLEO platform arena. So as we announced sometime last spring in ‘24, we won a program called DARPA Otter that is the development of a platform that we call Sabersat, which is a VLEO spacecraft.

And people started calling that spacecraft, because of how low that it orbits, an orbital drone, which then kind of triggered in our head this idea that the difference between airborne assets and space-based autonomous platforms is largely arbitrary from an employment perspective. And Sabersat is really kind of bridging that gap between space and airborne and platforms.

So we realized that by adding an unmanned aerial systems company like Edge we could provide that platform coverage from the surface of the Earth all the way to the surface of the moon and beyond. And that was really exciting to us because I think we're just starting to scratch the surface of what's possible when you start to have a vertically integrated company that has both these kind of platforms all in the same portfolio.

Morgan Brennan

I'm going to take a little bit. I'm going to transgress a little bit because you were just talking about very low Earth orbit. You and I actually had this conversation. We talked about that a little bit last year at the Space Symposium. But I mean, it's still, I think, a newer or at least it's seen as a newer concept. I think about the stratospheric spy balloon from China, which sort of shed a light on this sort of, you know, area, between air and space, if you will, and what that looks like and what securing that looks like. So when we do talk about very low Earth orbit, and we talk about your role in that, what does that involve?

Peter Cannito

Well, it involves basically getting closer to Earth for space assets, but while still far enough away to have strategic and tactical advantage. And the promise of VLEO is this idea that you can get closer, which means you can get higher resolution from a technological perspective. When you're doing Earth observation, you can receive stronger and have stronger signals.

So that's what VLEO really is about, is extending the range of orbits that you're operating in. That, of course, also adds resiliency. We believe that in space will be a hybrid architecture involving multiple orbits, from VLEO all the way through GEO and into ex-GEO such as cislunar. So, VLEO is adding a whole new technical capability to an already robust space market.

Morgan Brennan

So now with Edge Autonomy, what I think is fascinating is the fact that it already has drones and products that are deployed out in the marketplace, and not just with the U.S. military, but with international buyers as well perhaps most notably in being used in Ukraine on the battlefield.

Peter Cannito

That's right.

Morgan Brennan

So where does drone warfare go from here, especially at a time where in many cases, Ukraine has become this testbed of modern warfighting and where technology is taking us?

Peter Cannito

Yes. Well, so that's an excellent question. It’s going to continue to evolve and it's going to continue to advance. It's obviously going to be critical to a multi-domain or all-domain warfighting environment.

One of the things that we're really excited about where Edge Autonomy is currently positioned and how Redwire bringing space capabilities to Edge Autonomy, will increase advantage is they have some really interesting intellectual property around their battery technology that gives them extended endurance and range. In the UAS market, they have these groups from smallest to largest is Group 1 through 5, and Edge Autonomy operates in Group 2. The large ones tend to have really long range, a lot of capability like Predator, but they're also very expensive.

And of course, the smaller ones are cheaper, but are less capable. This extended endurance that Edge Autonomy’s platform brings to the table allows it, as a Group 2 UAS provider, to start taking on missions that have typically been reserved for the more advanced Group 3 capabilities but at a lower price point. But when you start looking at that additional endurance and range you run into, potentially, extending beyond your direct communication link.

And that's where space comes into play. So the combination of Redwire space-based assets and the Group 2 extended range that Edge Autonomy has allows us to strategically position ourselves to compete from a mission perspective for missions that are currently done by much more expensive UAS technologies, and that we believe will give us stronger demand and a competitive advantage over time.

Morgan Brennan

So now, if I take a step back this adds a new capability to an already burgeoning portfolio at Redwire. Let’s talk a little bit about some of the other businesses, because I know you have this really fascinating biotech business where you send PIL-BOX to Earth orbit, and you've worked with companies like Eli Lilly to grow crystals to further medicine and drug development. You are very involved in space manufacturing and satellites in general. So I guess just walk me through the portfolio more broadly. What you're excited about in 2025 and beyond.

Peter Cannito

It's a great question. So we have four primary growth principles, that we call protecting the core, scaling production, moving up the value chain and venture optionality.

And of course, protecting the core is about doing those fundamental things that Redwire has been successful doing for many decades - and that's selling these picks and shovels, if you will, for space. And we’ve got to make sure we never take our eye off the ball in being able to service our existing customers.

Scaling production is our principle as demand increases for space and now, unmanned aerial systems, we have to be able to intelligently scale our production to meet that increasing demand.

Moving up the value chain, which Edge Autonomy was a critical piece of that strategy, is that idea of now having this portfolio of platforms. Being more than just a merchant supplier, but having the ability to be a prime contractor, using this portfolio of platforms, whether in space, whether as unmanned aerial systems or the combination of both.

And then of course we have our venture optionality, which is our, in-space manufacturing, our microgravity development, and as you mentioned that includes our biotech development as well. We're really excited because if you think about that portfolio effect of having a really strong fundamental business around picks and shovels as being a base that gives us strong financial stability and operational resiliency, you kind of move up to that scaling; including the platforms all the way to having that venture optionality of having a breakout technology like the ability to print organs or the ability to do advanced drug manufacturing from space.

You can see that in Redwire, when you invest in Redwire, you get a very stable company that has the positioning to really scale, but also has a little bit of that venture aspect to it as well. And I think that’s exciting to a lot of our investors.

Morgan Brennan

And you are publicly traded, you went public, back in, what, 2021? Given the fact that we do talk about space, space is quote-unquote “hard.” Some of these, you know, some projects when it comes to space have long lead times. So what is it like to have to give quarterly earnings and be a publicly traded company and, you know, engage with investors when we are talking about some very technical, scientific, innovative products?

Peter Cannito

Well, so Elon Musk kind of helps us out with that, obviously, he's very visible in the community and so I think there are a lot of people in space right now and that public knowledge is certainly a tailwind for Redwire, because I think that the public writ large is more aware of what's going on in space than ever before. I mean, I think it's just consistently going out there quarter after quarter and educating people on what you're doing and then delivering on the things that you say you're going to do and we believe that if we continue to do that, that people understand it over time.

Morgan Brennan

It does seem like there is a lot of investor enthusiasm for space companies and specifically commercial space - and defense too like, I just think there's a lot more enthusiasm than I've ever seen before. And I wonder what you make of that and what a new administration coming in and expectations around perhaps, innovative policies to continue to propel space exploration and find lower cost options, whether it is on the military side or the space side. What all of that means for this.

Peter Cannito

Well, we believe and we have, regardless of the administration, that we're entering in the next golden age of space, there's just too many compelling use cases, for space, for Earth. And there's also, I believe, an overwhelming interest in the exploration aspects of space as well, to include returning to the moon to include, eventually, having a presence on Mars.

So, again, this second golden age of space, seems to be what the nation and quite frankly, the world, is rallying around. And, as that trend continues, that's very good for Redwire. So we're true believers in the benefit of space for Earth and also, the vision of humanity's drive to explore our universe and those are trends that we support and we're really proud and honored to be participating in.

Morgan Brennan

So you just announced this acquisition of Edge Autonomy that's expected to close sometime in the second quarter. What are the other milestones for the company this year?

Peter Cannito

Well, this is pretty transformational for us. So, we're going to put a lot of focus on this, while continuing to execute against our four fundamental principles of growth.

So I think you're going to see a lot more of the same, that you saw in the last year in terms of well-thought out, well-valued accretive acquisitions. You're going to see more advancements in our PIL-BOXes and microgravity development that we've talked about during each of our earnings calls.

You're going to see us continue to move up the value chain and maturing our platforms and going after and bidding much larger contracts focused on these platforms to include now, trying to position for opportunities to build a system-of-systems approach using the two domains of airborne and space working together. And of course, we'll never not focus on our existing customers and the foundational business of providing the picks and shovels that underpin this space trend.

So if you think about where we've positioned ourselves now with the addition of Edge Autonomy, I like to think about it in three fundamental areas: technical, financial and operational. We've talked a little bit about the technical in the sense that moving towards this trend of multi-domain warfighting, the financial, by doing this transaction and having a really robust, not only strong top line, but strong EBITDA projection, as well as we're forecasting that this transaction will make us free cash flow positive.

That gives us that strong financial foundation to ensure that we can execute our strategy over multiple years getting into that mode of self-funding - and that's a really advantageous place to be as, both a space company and a defense tech company.

And then lastly operational, we're going to be looking at, all the new, synergies that this, acquisition, has for us in terms of the geographic synergy of having a really strong critical mass in Europe, since Edge Autonomy has a strong presence in Latvia, and Redwire has a strong presence in Belgium and Luxembourg and most recently opened an office in Poland. And the other operational aspects of the deal to include shared manufacturing space and things of that ilk. So we're just going to do what we've always done and that is endeavor to follow up on the things that we've said we've been going to do in terms of these four growth pillars for the last year.

Morgan Brennan

Great. Final question for you - still acquisitive, I guess, looking out to the longer term, are there going to be other domains that you expand into beyond this?

Peter Cannito

Well, in terms of whether we expand into other domains or not, I can't say, but what I can say is that this being our 11th acquisition, I think it would be a surprise to nobody that M&A is a strategic core competency for Redwire. We think we've done it very successfully in the past. And, it will be an important part of a broad strategy, but, still an important part of our strategy going forward.

Morgan Brennan

Peter Cannito, CEO of Redwire. I appreciate the time today. Thank you.

Peter Cannito

Thank you.

Additional Information and Where to Find It

The definitive agreement entered into in connection with the proposed business combination described herein and a summary of material terms of the transaction will be provided in a Current Report on Form 8-K or Schedule 14A to be filed with the Securities and Exchange Commission (the “SEC”). Redwire will file with the SEC a proxy statement relating to a special meeting of Redwire’s stockholders (the “proxy statement”). STOCKHOLDERS ARE URGED TO CAREFULLY READ THE PROXY STATEMENT AND ANY OTHER RELEVANT DOCUMENTS TO BE FILED WITH THE SEC IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT REDWIRE, EDGE AUTONOMY, THE TRANSACTION AND RELATED MATTERS. Stockholders will be able to obtain free copies of the proxy statement and other documents filed with the SEC by the parties through the website maintained by the SEC at www.sec.gov. In addition, investors and stockholders will be able to obtain free copies of the proxy statement and other documents filed with the SEC by the parties on investor relations section of Redwire’s website at redwirespace.com.

Participants in the Solicitation

Redwire and its directors and executive officers may be deemed to be participants in the solicitation of proxies from the stockholders of Redwire in respect of the proposed business combination contemplated by the proxy statement. Information regarding the persons who are, under the rules of the SEC, participants in the solicitation of the stockholders of Redwire, respectively, in connection with the proposed business combination, including a description of their direct or indirect interests, by security holdings or otherwise, will be set forth in the proxy statement when it is filed with the SEC. Information regarding Redwire’s directors and executive officers is contained in Redwire’s Annual Report on Form 10-K for the year ended December 31, 2023 and its Proxy Statement on Schedule 14A, dated April 22, 2024, which are filed with the SEC.

No Offer or Solicitation

This communication is not intended to and does not constitute an offer to sell or the solicitation of an offer to subscribe for or buy or an invitation to purchase or subscribe for any securities or the solicitation of any vote in any jurisdiction pursuant to the proposed business combination or otherwise, nor shall there be any sale, issuance or transfer of securities in any jurisdiction in contravention of applicable law.

Forward-Looking Statements

Readers are cautioned that the statements contained in this communication regarding expectations of our performance or other matters that may affect our or the combined company’s business, results of operations, or financial condition are “forward-looking statements” as defined by the “safe harbor” provisions in the Private Securities Litigation Reform Act of 1995. Such statements are made in reliance on the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements, other than statements of historical fact, included or incorporated in this communication, including statements regarding our or the combined company’s strategy, financial projections, including the prospective financial information provided in this communication, financial position, funding for continued operations, cash reserves, liquidity, projected costs, plans, projects, awards and contracts, and objectives of management, the entry into the potential business combination, the expected benefits from the proposed business combination, the expected performance of the combined company, the expectations regarding financing the proposed business combination, among others, are forward-looking statements. Words such as “expect,” “anticipate,” “should,” “believe,” “target,” “continued,” “project,” “plan,” “opportunity,” “estimate,” “potential,” “predict,” “demonstrates,” “may,” “will,”

“could,” “intend,” “shall,” “possible,” “forecast,” “trends,” “contemplate,” “would,” “approximately,” “likely,” “outlook,” “schedule,” “pipeline,” and variations of these terms or the negative of these terms and similar expressions are intended to identify these forward-looking statements, but the absence of these words does not mean that a statement is not forward looking. These forward-looking statements are not guarantees of future performance, conditions or results. Forward-looking statements are subject to a number of risks and uncertainties, many of which involve factors or circumstances that are beyond our control.

These factors and circumstances include, but are not limited to: (1) risks associated with the continued economic uncertainty, including high inflation, supply chain challenges, labor shortages, increased labor costs, high interest rates, foreign currency exchange volatility, concerns of economic slowdown or recession and reduced spending or suspension of investment in new or enhanced projects; (2) the failure of financial institutions or transactional counterparties; (3) Redwire’s limited operating history and history of losses to date as well as the limited operating history of Edge Autonomy and the relatively novel nature of the drone industry; (4) the inability to successfully integrate recently completed and future acquisitions, including the proposed business combination with Edge Autonomy, as well as the failure to realize the anticipated benefits of the transaction or to realize estimated projected combined company results; (5) the development and continued refinement of many of Redwire’s and the combined company’s proprietary technologies, products and service offerings; (6) competition with new or existing companies; (7) the possibility that Redwire’s expectations and assumptions relating to future results and projections with respect to Redwire or Edge Autonomy may prove incorrect; (8) adverse publicity stemming from any incident or perceived risk involving Redwire, Edge Autonomy, the combined company, or their competitors; (9) unsatisfactory performance of our and the combined company’s products resulting from challenges in the space environment, extreme space weather events, the environments in which drones operate, including in combat or other areas where hostilities may occur, or otherwise; (10) the emerging nature of the market for in-space infrastructure services and the market for drones and related services; (11) inability to realize benefits from new offerings or the application of our or the combined company’s technologies; (12) the inability to convert orders in backlog into revenue; (13) our and the combined company’s dependence on U.S. and foreign government contracts, which are only partially funded and subject to immediate termination, or which may be influenced by the level of military activities and related spending such as in or with respect to the war in Ukraine; (14) the fact that we are and the combined company will be subject to stringent economic sanctions, and trade control laws and regulations; (15) the need for substantial additional funding to finance our and the combined company’s operations, which may not be available when needed, on acceptable terms or at all; (16) the dilution of existing holders of our common stock that will result from the issuance of additional shares of common stock as consideration for the acquisition of Edge Autonomy, as well as the issuance of common stock in any offering that may be undertaken in connection with such acquisition; (17) the fact that the issuance and sale of shares of our Series A Convertible Preferred Stock has reduced the relative voting power of holders of our common stock and diluted the ownership of holders of our capital stock; (18) the ability to achieve the conditions to cause, or timing of, any mandatory conversion of the Series A Convertible Preferred stock into common stock; (19) the fact that AE Industrial Partners and Bain Capital have significant influence over us, which could limit your ability to influence the outcome of key transactions; (20) provisions in our Certificate of Designation with respect to our Series A Convertible Preferred Stock may delay or prevent our acquisition by a third party, which could also reduce the market price of our capital stock; (21) the fact that our Series A Convertible Preferred Stock has rights, preferences and privileges that are not held by, and are preferential to, the rights of holders of our other outstanding capital stock; (22) the possibility of sales of a substantial amount of our common stock by our current stockholders, as well as the equity owners of Edge Autonomy following consummation of the transaction, which sales could cause the price of our common stock and warrants to fall; (23) the impact of the issuance of additional shares of Series A Convertible Preferred Stock as pay in kind dividends on the price and market for our common stock; (24) the volatility of the trading price of our common stock and warrants; (25) risks related to short sellers of our common stock; (26) Redwire’s or the combined company’s inability to report our financial condition or results of operations accurately or timely as a result of identified material weaknesses in internal control over financial reporting, as well as the possible need to expand or improve Edge Autonomy’s financial reporting systems and controls; (27) the possibility that the closing conditions under the merger agreement necessary to consummate the merger between Redwire and Edge Autonomy will not be satisfied; (28) the effect of any announcement or pendency of the proposed business combination on Redwire’s or Edge Autonomy’s business relationships, operating results and business generally; (29) risks that the proposed business combination disrupts current plans and operations of Redwire or Edge Autonomy; (30) the ability of

Redwire or the combined company to raise financing in connection with the proposed business combination or to finance its operations in the future; (31) the impact of any increase in the combined company’s indebtedness incurred to fund working capital or other corporate needs, including the repayment of Edge Autonomy’s outstanding indebtedness and transaction expenses incurred to acquire Edge Autonomy, as well as debt covenants that may limit the combined company’s activities, flexibility or ability to take advantage of business opportunities, and the effect of debt service on the availability of cash to fund investment in the business; (32) the ability to implement business plans, forecasts and other expectations after the completion of the proposed transaction, and identify and realize additional opportunities; (33) costs related to the transaction; and (34) other risks and uncertainties described in our most recent Annual Report on Form 10-K and Quarterly Reports on Form 10-Q and those indicated from time to time in other documents filed or to be filed with the SEC by Redwire. The forward-looking statements contained in this communication are based on our current expectations and beliefs concerning future developments and their potential effects on us. If underlying assumptions to forward-looking statements prove inaccurate, or if known or unknown risks or uncertainties materialize, actual results could vary materially from those anticipated, estimated, or projected. The forward-looking statements contained in this communication are made as of the date of this communication, and Redwire disclaims any intention or obligation, other than imposed by law, to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Persons reading this communication are cautioned not to place undue reliance on forward-looking statements.

Use of Data

Industry and market data used in this communication have been obtained from third-party industry publications and sources, as well as from research reports prepared for other purposes. Redwire or Edge Autonomy have not independently verified the data obtained from these sources and cannot assure you of the data’s accuracy or completeness. This data is subject to change. Statements other than historical facts, including, but not limited to, those concerning market conditions or trends, consumer or customer preferences or other similar concepts with respect to Redwire, Edge Autonomy and the expected combined company, are based on current expectations, estimates, projections, targets, opinions and/or beliefs of Redwire or, when applicable, of one or more third-party sources. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. In addition, no representation or warranty is made with respect to the reasonableness of any estimates, forecasts, illustrations, prospects or returns, which should be regarded as illustrative only, or that any profits will be realized. The metrics regarding select aspects of Redwire's, Edge Autonomy’s and the expected combined company’s operations were selected by Redwire or its subsidiaries on a subjective basis. Such metrics are provided solely for illustrative purposes to demonstrate elements of Redwire's businesses, are incomplete, and are not necessarily indicative of Redwire’s, Edge Autonomy’s or their subsidiaries’ performance or overall operations. There can be no assurance that historical trends will continue.

The Edge Autonomy financial information, including non-GAAP measures, for the last twelve months ended September 30, 2024 and year ended December 31, 2023 included in this communication is unaudited and subject to change. The historical financial information, including any related non-GAAP information, for Edge Autonomy is subject to the finalization of year-end financial and accounting procedures (which are in process of being performed) and should not be viewed as a substitute for audited results prepared in accordance with U.S. generally accepted accounting principles. The actual results may be materially different from the unaudited results, and therefore undue reliance should not be placed on the unaudited information.

Use of Projections

The financial outlook and projections, estimates and targets in this communication are forward-looking statements that are based on assumptions that are inherently subject to significant uncertainty and contingencies, many of which are beyond Redwire’s or Edge Autonomy’s control. Neither Redwire nor Edge Autonomy’s independent auditors have audited, reviewed, compiled or performed any procedures with respect to the financial projections for purposes of inclusion in this communication, and, accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purposes of this communication. While all financial projections, estimates and targets are necessarily speculative, Redwire believes that the preparation of prospective financial information involves increasingly higher levels of uncertainty the further out the projection, estimate or target extends from the date of preparation. The assumptions and estimates underlying the projected, expected or target results for Redwire,

Edge Autonomy and the combined company are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the financial projections, estimates and targets. The inclusion of financial projections, estimates and targets in this communication should not be regarded as an indication that Redwire, or its representatives, considered or consider the financial projections, estimates or targets to be a reliable prediction of future events. Further, inclusion of the prospective financial information in this communication should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved.

Non-GAAP Financial Information

This communication contains financial measures that have not been prepared in accordance with United States Generally Accepted Accounting Principles (“U.S. GAAP”). These financial measures include forecasted Adjusted EBITDA and Free Cash Flow for Redwire assuming completion of the acquisition of Edge Autonomy.

Non-GAAP financial measures are used to supplement the financial information presented on a U.S. GAAP basis and should not be considered in isolation or as a substitute for the relevant U.S. GAAP measures and should be read in conjunction with information presented on a U.S. GAAP basis. Because not all companies use identical calculations, our presentation of Non-GAAP measures may not be comparable to other similarly titled measures of other companies. We encourage investors and stockholders to review our financial statements and publicly-filed reports in their entirety and not to rely on any single financial measure. As soliciting material that is filed pursuant to Rule 14a-12, this communication is exempt from the requirements of Regulation G and Item 10(e) of Reg. S-K with respect to Non-GAAP financial measure disclosure.

Adjusted EBITDA is defined as net income (loss) adjusted for interest expense, net, income tax expense (benefit), depreciation and amortization, impairment expense, acquisition deal costs, acquisition integration costs, acquisition earnout costs, purchase accounting fair value adjustment related to deferred revenue, severance costs, capital market and advisory fees, litigation-related expenses, write-off of long-lived assets, gains on sale of joint ventures, equity-based compensation, committed equity facility transaction costs, debt financing costs, and warrant liability change in fair value adjustments. Free Cash Flow is computed as net cash provided by (used in) operating activities less capital expenditures.

We use Adjusted EBITDA to evaluate our operating performance, generate future operating plans, and make strategic decisions, including those relating to operating expenses and the allocation of internal resources. We use Free Cash Flow as a useful indicator of liquidity to evaluate our period-over-period operating cash generation that will be used to service our debt, and can be used to invest in future growth through new business development activities and/or acquisitions, among other uses. Free Cash Flow does not represent the total increase or decrease in our cash balance, and it should not be inferred that the entire amount of Free Cash Flow is available for discretionary expenditures, since we have mandatory debt service requirements and other non-discretionary expenditures that are not deducted from this measure.